Tariff Summary

Last Wednesday, the Trump administration unveiled a set of tariffs on most U.S. trading partners that was more aggressive than most market participants expected. A 10% baseline levy was imposed on almost all trading partners that went into effect over the weekend, with Mexico and Canada excluded but still subject to previously announced 25% tariffs. Additional duties described as “reciprocal” determined by a custom calculation were applied to 60 trading partners with the largest trade imbalances with the U.S. effective April 9. Notable trading partners targeted with the highest tariff rates are China (54%), Vietnam (46%), the European Union (34%), and India (27%). Aluminum, steel, lumber, semiconductors and pharmaceuticals were exempted from the new round of tariffs. According to Capital Economics, if left unchanged, the tariffs would increase the effective average tariff rate from 2.3% in 2024 to 23%-24% in 2025. This would be the highest level since 1900.

The Trump administration has said their actions are aimed at restoring what they view as fair international trade while raising revenue to help offset tax cuts planned for later this year. Substantial tariff revenue could also potentially reduce the growth trajectory of the national debt. More broadly, their aim is to restore domestic manufacturing by incentivizing domestic goods production. Strategically, the onshoring of certain manufacturing processes would strengthen the U.S. military-industrial base.

Investors will be looking for reports on progress in bilateral negotiations between the Trump administration and trade partners to lower the surprisingly high tariff rates applied on a group of 60 nations with large trade imbalances last week. Any retaliatory measures against the U.S. would likely be greeted negatively by markets.

Market Reaction

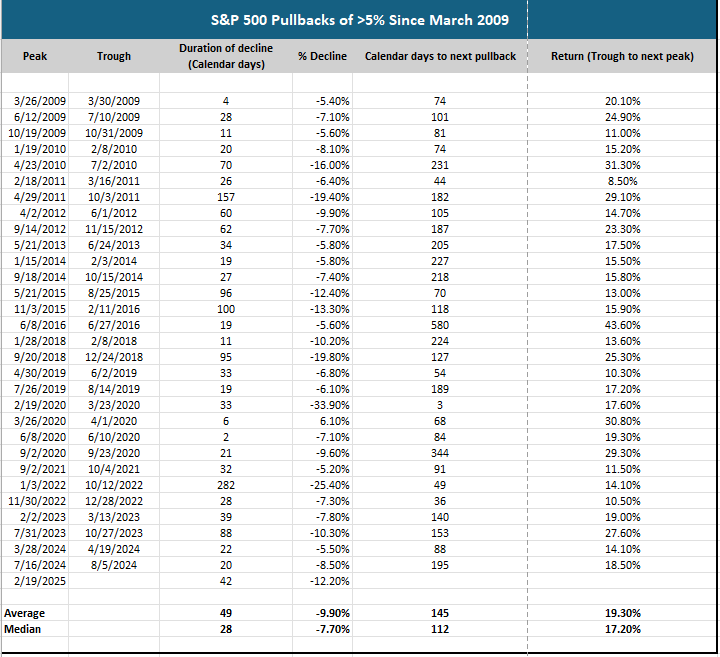

U.S. markets declined sharply following the announcement with the Dow Jones Industrial Average, S&P 500, and Nasdaq all down 6%-8% since last Tuesday’s close as of Friday morning. The S&P 500 trading reflected a correction of about 15% from its intraday high of 6,147.43 on February 19. Within the S&P 500, the defensive consumer staples, utilities and healthcare sectors have been the benchmark’s top performing groups. More cyclical sectors, including energy, technology and consumer discretionary have been among the weakest areas of the index. Packaged foods, household products, regulated electric utilities, pharmaceuticals, insurers, financial exchanges, health insurers, and healthcare distributors have displayed the most resilience recently. Apparel and footwear retailers, home furnishings retailers, cruise line operators, airlines, banks, and most semiconductor companies suffered the steepest declines.

Treasury yields in the 2-to-10-year portion of the yield curve fell between 20 and 25 basis points (bps) in recent days, with the 10-year note yield pushing below 4% for the first time since mid-October. WTI crude oil has plunged 12% to $62/barrel amid a combination of growth concerns and an unexpected increase in production quotas from OPEC and its production partners. Gold has dipped about 2% but is still within 4% of its all-time closing high Wednesday.

Friday morning’s March nonfarm payrolls report was stronger than expected. There were 228,000 net additions compared to the median Bloomberg estimate of 140,000, yet combined payroll gains in January and February were downwardly revised by 49,000. Total government payrolls increased by 19,000, with state and local jobs up 23,000 offset by a 4,000 loss of federal government positions. The unemployment rate ticked up to 4.2%, while average hourly wage growth was subdued at 3.8%. Market participants are likely looking through this morning’s decent payroll data, however, and projecting weakness in April.

Where Do We Go From Here?

Since mid-February, a more defensive risk stance and broader diversification have benefited portfolios, given 1) signs of slowing in select areas of the domestic economy, 2) elevated policy uncertainty around tariffs and government spending, and 3) U.S. large-cap index-level valuations that are full—although not necessarily extended—relative to long-term history. Looking ahead, we acknowledge a weaker fiscal impulse in the U.S. in 2025 compared to stimulus-heavy years of 2021-2024, alongside continued uncertainty about trade policy and government spending.

Yet, we do not think it is time to make significant shifts toward risk-off positioning in investment portfolios given:

1) Overall economic data remains mixed (weak survey data, signs of stability/strength remain in various hard data, including private payrolls, initial jobless claims, retail sales, etc.)

2) Corporate profit growth expectations and company guidance have softened but not rolled over.

3) The Federal Reserve still has ample room to ease policy with further rate cuts and balance sheet expansion.

Historically, deep and prolonged bear markets tend to coincide with a significant contraction in corporate earnings, which puts pressure on employment and capital expenditures. Importantly, meaningful declines in corporate earnings are rare outside of recessionary periods. Although the risks have risen over the past few months, a US recession is not a foregone conclusion. The recent 15% peak-to-trough correction in the S&P 500 that began in mid-February reflects the market’s attempt to price in higher odds of an economic slowdown or perhaps a mild recession. As a result, we anticipate risk asset markets will remain choppy and possibly trend sideways to lower over a near-term time frame. At the same time, equity valuations have moderated, which increases the potential for more substantial long-term returns once a new cycle begins. In this market environment with markets pricing slower growth and sticky inflation, we expect diversification across asset classes to be an investor’s best friend.

We expect exposure to defensive assets (high-quality bonds, gold, cash) will continue to dull periodic drawdowns in portfolios as volatility is likely to remain elevated for the foreseeable future. In contrast, an appropriately sized allocation to growth assets (equities) enables portfolios to participate in market upside if/when the fiscal and trade policy environments stabilize. Looking further out (second half of 2025), we expect the Trump administration to shift its focus away from trade policy and toward the more growth-positive aspects of its agenda, including tax cuts, supporting domestic manufacturing, and deregulation.

As always, we remind clients of the long-term nature of their investments and the importance of avoiding market timing. History shows that equity markets tend to recover and normalize following periods of steep declines. Maintaining discipline during volatile periods is key. Having a clear and reasonable investment objective is critical because it determines how much risk (volatility) an investor is willing and able to tolerate. The objective should be aligned with an investor’s time horizon, distribution requirements, and risk tolerance. For accounts with expected distributions over the next 3-6 months, we recommend raising cash into market rallies and maintaining elevated cash balances until conditions become more favorable.

In the short term, we expect bouts of continued pressure on U.S. stocks along with periods of potentially surprising price strength depending on the headlines and direction of trade, fiscal, and monetary policy. The longer the tariffs as currently exist remain in place, we would anticipate rising odds of a slowing in the U.S. economy and softness in the domestic business cycle. With this in mind, we anticipate recommending moderate shifts toward higher quality asset classes to reflect the changing tone of the policy and market backdrops. As always, we will be watching key market, economic, and sentiment indicators in coming weeks and months to gauge if a more defensive posture in client portfolios is advisable.

What Else We’re Keeping an Eye On

Federal Budget Dealmaking

Early Saturday morning, the U.S. Senate passed a budget resolution in a 51-48 vote (with two GOP senators opposed) that is viewed as an important first step in passing a tax and spending bill supported by President Trump. The resolution, which would enable Congress to vote on a budget bill, will head to the House of Representatives this week. It could come under fire from fiscally conservative members of the Freedom Caucus. In its current form, the package would extend the 2017 tax cuts, implement $1.5 trillion of additional tax cuts over the next ten years, and raise the federal debt ceiling by $5 trillion.

March Inflation Readings

With recently implemented tariff hikes, the pace of price increases in core goods categories will be under the microscope when the Bureau of Labor Statistics reports the Consumer Price Index (CPI) data for March on Thursday morning. According to the median consensus in a Bloomberg survey, the overall core reading is expected to be 0.3% (vs. 0.2% last month), while a year-over-year rate of 3.0% (vs. 3.1% in February) is anticipated. High frequency data in recent weeks have pointed to softening used-car inflation despite concerns about sharply higher prices for new cars due to tariffs.

IMPORTANT INFORMATION: This material is for information purposes only. The views expressed are those of the author(s) as of the date noted and not necessarily of the Corporation and are subject to change based on market or other conditions without notice. The information should not be construed as investment advice or a recommendation to buy or sell any security or investment product. It does not take into account an investor’s particular objectives, risk tolerance, tax status, investment horizon, or other potential limitations. All material has been obtained from sources believed to be reliable, but the accuracy cannot be guaranteed.

Legal, Investment and Tax Notice: This information is not intended to be and should not be treated as legal advice, investment advice or tax advice. Readers, including professionals, should under no circumstances rely upon this information as a substitute for their own research or for obtaining specific legal or tax advice from their own counsel.